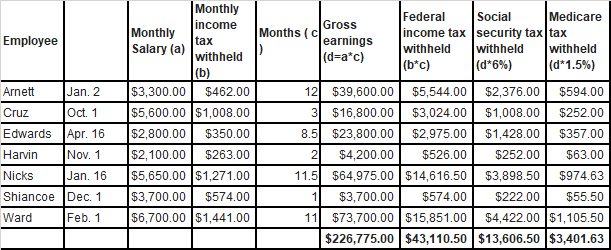

Single Column Cash Book.

- Get link

- X

- Other Apps

A single column cash book is a simple bookkeeping ledger used to record all cash transactions that occur in a business. It has a single column for each transaction, which is used to record either debit or credit entries.

Here is an example of a single column cash book:

| Date | Particulars | L.F. | Amount |

|---|---|---|---|

| 1/1 | Balance b/d | 5000 | |

| 1/3 | Sales | 1001 | 2500 |

| 1/5 | Rent paid | 1002 | 1200 |

| 1/8 | Cash deposited | 3000 | |

| 1/11 | Purchase | 1003 | 2000 |

| 1/15 | Wages paid | 1004 | 1500 |

| 1/22 | Cash withdrawn | 1000 | |

| 1/31 | Balance c/d | 8300 |

In this example, the first row shows the opening balance. The "L.F." column is used to record the page number of the ledger where the transaction is recorded.

On January 3rd, a sale was made for 2,500 and recorded as a credit entry. On January 5th, rent was paid for 1,200 and recorded as a debit entry. On January 8th, cash of 3,000 was deposited and recorded as a credit entry.

On January 11th, a purchase was made for 2,000 and recorded as a debit entry. On January 15th, wages were paid for 1,500 and recorded as a debit entry.

On January 22nd, cash of 1,000 was withdrawn and recorded as a debit entry. Finally, on January 31st, the closing balance was recorded.

This example demonstrates how a single column cash book can be used to record all cash transactions and maintain accurate records of a business's financial transactions. However, unlike a double column cash book, a single column cash book does not allow for easy tracking of cash inflows and outflows from different sources.

- Get link

- X

- Other Apps

Comments

Post a Comment